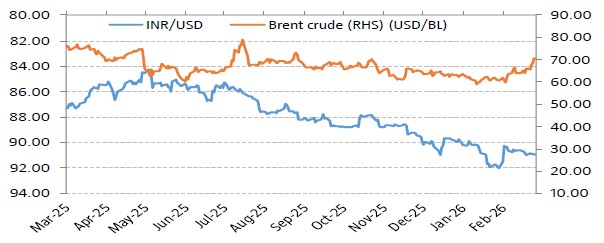

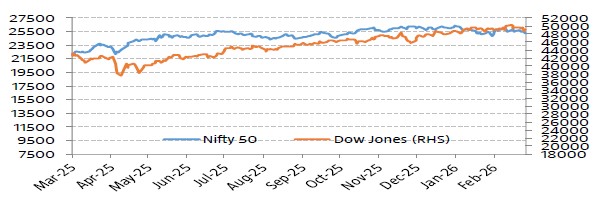

Equity Markets - India & US

Bellwether indices, Nifty 50 and BSE Sensex decreased marginally during the month by 0.56% and 1.19% respectively amid increase in crude oil prices coupled with weakness in the rupee and rising tensions between the U.S. and Iran. Worries about disruptions related to artificial intelligence also kept investors on the edge. Foreign Institutional Investors (FIIs) were net buyers in Indian equities to the tune of ` 22,614.65 crore. Gross Goods and Services Tax (GST) collections in February 2026 stood at Rs. 1.83 trillion, representing a 8.1% rise on a yearly basis and this points towards the growing trajectory of the Indian economy. Dow Jones increased by 1.73% from previous month.

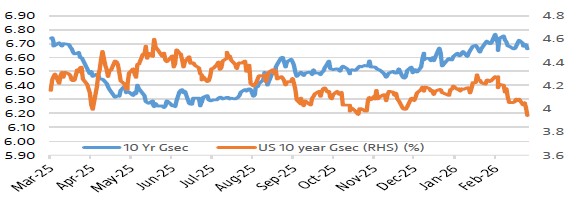

Interest Rate Movement (%) - India & US

Yield on the 10-Year benchmark paper marginally decreased, closing at 6.66% on Feb’26 vs 6.696% on Jan’26 after a strong response at the weekly state debt auction. Indian states collectively raised Rs. 46,100 crore through bond sales, surpassing the planned issuance of Rs. 44,550 crore and indicating robust investor demand. US 10 year G-Sec closed lower at 3.9375 on Feb’26 vs 4.2355 on Jan’26.

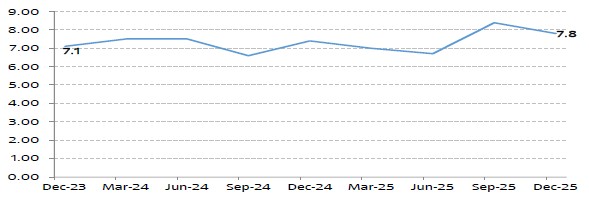

India GDP Growth Rate

India’s GDP grew 7.8% for Q3 FY26 vs 8.23% for Q2 FY26, indicating a marginal moderation in economic growth during the quarter. On the sectoral front, the growth of Manufacturing sector rose to 13.3% in Q3 of FY26 from 10.8% in the same quarter of the previous fiscal year, supported by improved industrial activity and production levels. The growth of Agriculture, Livestock, Forestry & Fishing slowed to 1.4% in Q3 of FY26 compared to 5.8% rise in Q3 of FY25, reflecting weaker output in the agricultural sector during the period.